Beyond Bambu Lab and Creality: Inside the 53% Surge in Budget 3D Printer Sales

Market intelligence firm Context reports that the global 3D printing sector is finally shaking off its two-year slump, fueled almost entirely by an explosion in entry-level systems.

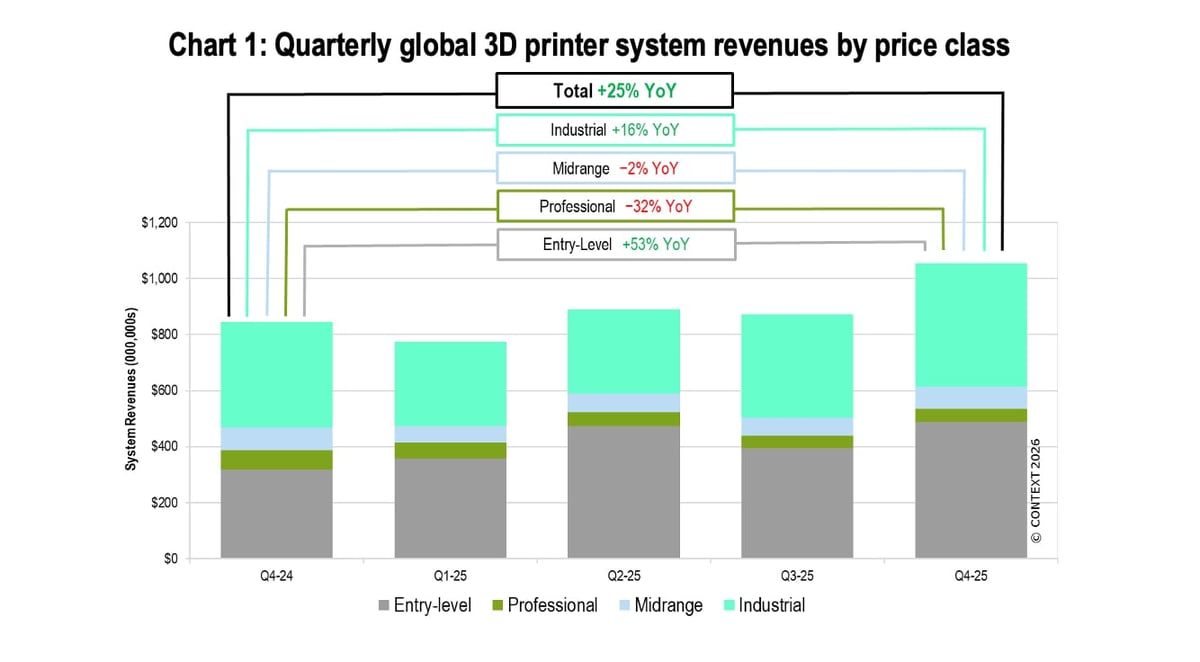

If it feels like everyone is suddenly buying a 3D printer, the numbers back it up. Driven by a massive 47% fourth-quarter surge in budget-friendly, entry-level model sales, the global 3D printing market exploded at the end of 2025. Desktop 3D printing is officially going mainstream, pulling the entire industry out of a two-year slump according to the latest data from market intelligence firm Context, which is bolstered by other recent market reports by AM Research and Wohlers Associates.

Big Machines, Big Comeback: Industrial 3D Printing Wakes Up

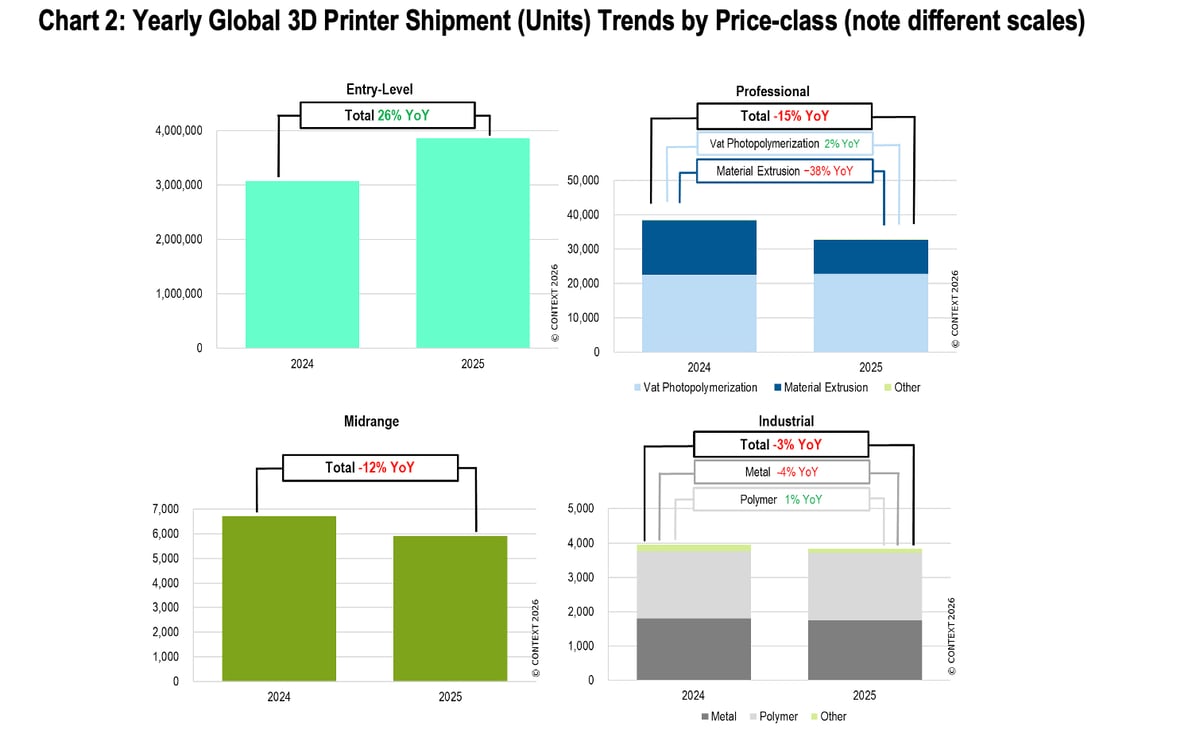

In polymers, shipments of industrial polymer printers rose 23% during the quarter. That growth was led by a 39% increase in vat photopolymerization systems from vendors including Carbon and UnionTech.

In metals, shipments rose 5% for the quarter, with metal powder bed fusion systems standing out. Unit shipments in that category increased 24%.

Chinese companies BLT, Eplus3D, ZRapid Tech and Farsoon led the market in metal powder bed fusion unit share, while EOS and Nikon SLM Solutions remained ahead in revenue share.

Entry-level Printers Become the Market’s Main Engine

The entry-level category, which includes systems priced below $2,500, continued to be the industry’s biggest growth story. Shipments in this segment rose 47% in the fourth quarter and 26% across all of 2025.

According to Context, entry-level systems are now a major financial driver for the 3D printing industry. Chinese vendors made up more than 90% of global shipments in this category during 2025.

Bambu Lab led the segment with a 37% market share, followed by Creality, Elegoo, and Anycubic. Context also said the category is attracting more strategic capital. Creality is preparing for an initial public offering, while other major players are reportedly drawing investment from Chinese financial firms.

Midrange and Professional Systems Stay Under Pressure

In the midrange category, covering systems priced from $20,000 to $100,000, global shipments fell 6% year over year in the fourth quarter and 12% for the full year. Context said this part of the market was also affected by consolidation and mergers during 2025.

The professional segment, which includes systems priced between $2,500 and $20,000, saw shipments drop 12% in the quarter and 15% for the full year. Vat photopolymerization accounted for 71% of products shipped in this class, and Formlabs held the top market share for the year at 38%.

The Unstoppable Rise of Chinese 3D Printer Brands

Context said China has further established itself as a center of technical ingenuity in consumer 3D printing. In industrial systems, UnionTech stood out as a growth driver in metals, helped by demand from the shoe-mold market.

“The hype of years past has largely been replaced by a rigorous focus on key verticals and strategic areas of growth,” says Chris Connery, vice president of global analysis at Context.

What to Expect in 2026: More Growth

Looking ahead, Context expects growth in every price segment in 2026. Entry-level systems are forecast to grow the fastest, while industrial shipments are expected to post near double-digit percentage gains.

The firm pointed to several factors behind that outlook, including loosening U.S. interest rates, strength in China’s domestic market, and continued momentum in aerospace and defense. Growth in the professional and midrange categories is expected to be more modest.

You May Also Like:

License: The text of "Beyond Bambu Lab and Creality: Inside the 53% Surge in Budget 3D Printer Sales" by All3DP Pro is licensed under a Creative Commons Attribution 4.0 International License.